Understanding and managing your credit reports is crucial, as they play a vital role in many financial decisions made by creditors, insurers, employers, landlords, and utility companies. These reports provide a comprehensive overview of your financial history, including residential history, bill payments, and public records.

Unfortunately, errors in credit reports are more common than many might think, with studies indicating that a significant number of consumers have inaccuracies in their reports. These mistakes can lead to serious financial consequences, such as denial of credit or higher interest rates, which underscores the importance of identifying and disputing any errors.

Given the potential impact of inaccuracies on your financial wellbeing, it’s important to regularly review your credit reports and be proactive about correcting any errors. The Fair Credit Reporting Act (FCRA) supports consumers by ensuring credit bureaus offer a dispute resolution process.

This guide will walk you through the steps to effectively dispute errors on your credit report, from identifying inaccuracies to drafting a dispute letter and following up with credit bureaus. Understanding your rights under the FCRA and the common causes of credit report errors can empower you to maintain the accuracy of your financial records and protect your financial health.

The Importance of Disputing Credit Report Errors

While it’s common knowledge that credit reports play a significant role in various aspects of our financial lives, many consumers are unaware of the prevalence of errors within these reports.

According to the Consumer Financial Protection Bureau, one in five people have at least one error on their credit reports. Other studies have pointed out that up to 79% of consumer credit reports contain some type of mistake. This means that nearly four out of five individuals potentially have erroneous information on their credit reports, a fact that is as shocking as it is concerning.

The implications of such errors can be severe. Over 25% of credit report errors are serious enough to result in the denial of credit or an increase in interest rates. In the context of a mortgage, a good credit score could save you up to $100,000 over the life of a $250,000 loan.

If a credit bureau inaccurately reports your information, it could cost you an additional $100,000 on a 30-year mortgage, underscoring the importance of disputing credit report errors.

Ready to Raise Your Credit Score?

Learn how credit repair professionals can assist you in disputing inaccuracies on your credit report.

Know Your Rights: The Fair Credit Reporting Act (FCRA)

Considering the consequences of credit report errors, it’s a good idea to review your credit report periodically. Thankfully, the law is on your side. The United States government enacted the Fair Credit Reporting Act (FCRA), which mandates the three major credit bureaus to provide accurate information about you.

The FCRA also stipulates that these credit bureaus must have a dispute process in place to allow consumers to challenge any errors on their credit reports. If you challenge an item on your credit report, the credit bureau must notify the information provider, who then has 30 to 45 days to verify the item’s accuracy.

If they cannot verify it, they must correct it or remove it from your credit report. Once corrections are made, the credit bureau is obliged to inform anyone who has received your credit report in the past six months.

Common Causes of Errors on Credit Reports

Despite rigorous processes and regulations, errors can still creep into your credit reports. The causes of these errors are manifold. Financial institutions such as lenders, credit card issuers, and collection agencies sometimes report inaccurate information. Mistakes happen, they are, after all, human.

In other instances, mix-ups occur due to similar names or Social Security numbers. There are cases where a family member’s account details erroneously appear on a person’s credit report due to name similarities. Identity theft is another cause of credit report errors. If your Social Security number is stolen and used to open a credit account, it might appear on your credit report.

Another common error is the re-aging of accounts, which occurs when debt collectors pass your accounts around. These mistakes are all too common and should be disputed.

The Process of Disputing an Error on Your Credit Report

The dispute process can be conducted via mail, phone, or online. However, the most effective way to initiate a dispute is by sending a certified mail with a return receipt requested. This method allows you to keep a record of all correspondence with the credit bureau. It’s worth noting that disputing online via the credit bureau’s website might cause you to give up some of your rights.

1. Check Your Credit Report for Errors

The first step to disputing credit report errors is to obtain copies of your credit reports. Each of the three credit bureaus — Equifax, Experian, and TransUnion — are required by law to provide you with one free credit report every 12 months. Once you have these reports, dedicate some time to thoroughly reviewing them.

Ensure that all the information, including your personal details, is accurate. Look for any negative accounts on each credit report. Do you see anything questionable? If so, you’re entitled to dispute the account that contains the error.

2. Send a Credit Dispute Letter

The Consumer Financial Protection Bureau recommends contacting the credit bureaus that are reporting the errors. The most effective way to do this is through written correspondence. Importantly, filing a dispute doesn’t hurt your credit scores.

You can find sample dispute letters online that can guide you through the process. Alongside your letter, you may also include a copy of your credit report or any other documentation you think might be helpful, though this is not strictly necessary.

Each credit bureau also provides a credit bureau dispute form on their respective websites. Nevertheless, a personalized letter is often more impactful and advisable.

3. Wait for the Credit Bureau Investigation and Response

After a credit bureau receives notice of a dispute, they must conduct an investigation. The credit card company, lender, or other data furnisher associated with the disputed account also has to investigate the claim. They must then report their findings back to the credit bureau.

If inaccurate or incomplete information is found in the disputed account, the creditor must inform all three credit bureaus. In some instances, the creditor might fail to respond to the credit bureau. In such cases, the credit bureau is required to remove the disputed item from your credit report.

Typically, you can expect to hear back from the credit bureau about 30 to 45 days after they receive your dispute letter. However, you may receive the results of your dispute earlier in some cases.

Dispute Addresses & Phone Numbers for the Three Major Credit Bureaus

Equifax

Address:

Equifax Information Services LLC

P.O. Box 740256

Atlanta, GA 30374-0256

Phone number: (800) 685-1111

Experian

Address:

Experian

P.O. Box 4500

Allen, TX 75013

Phone number: (888) 397-3742

TransUnion

Address:

TransUnion LLC

Consumer Dispute Center

P.O. Box 2000

Chester, PA 19016

Phone number: (800) 916-8800

The Importance of Follow-Up

If you don’t receive the desired dispute results or your letter goes unanswered, you’ll need to follow up. If there’s no response within 30–40 days, send a follow-up letter. You can also file a formal complaint with the Federal Trade Commission (FTC).

Although the FTC doesn’t resolve individual consumer disputes, keeping a copy of the filed complaint can serve as evidence if you decide to sue the credit bureau for failure to comply with the law.

Getting Professional Help

Disputing credit report errors can be a daunting and time-consuming task. If you prefer professional assistance or simply don’t have the time, consider hiring one of the top credit repair services. Credit Saint, for example, has a proven track record of effectively removing incorrect entries for countless clients.

They know how to follow up with creditors and credit bureaus, especially when these entities are uncooperative. For optimal results, consider employing their services.

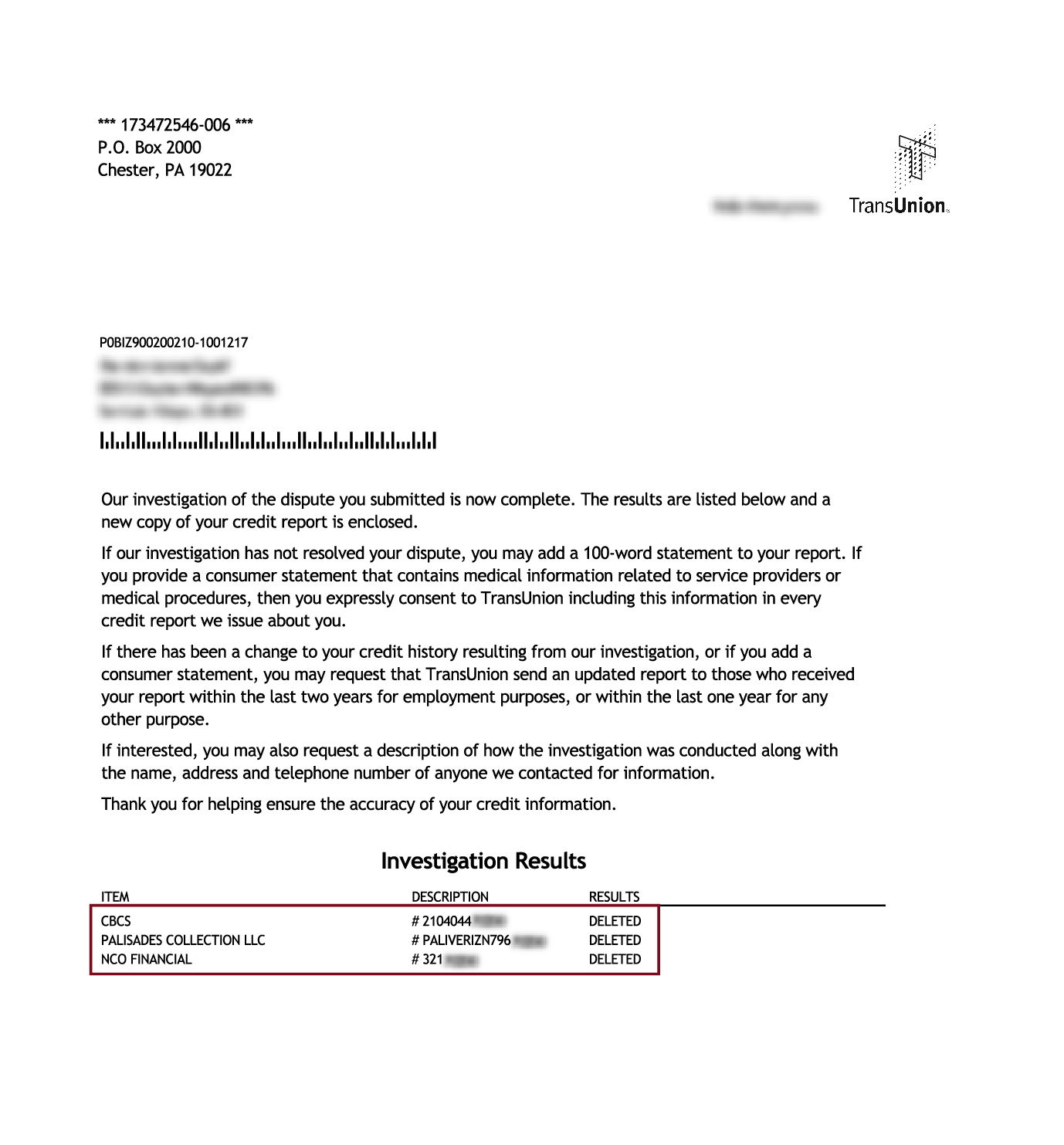

Collections Removed:

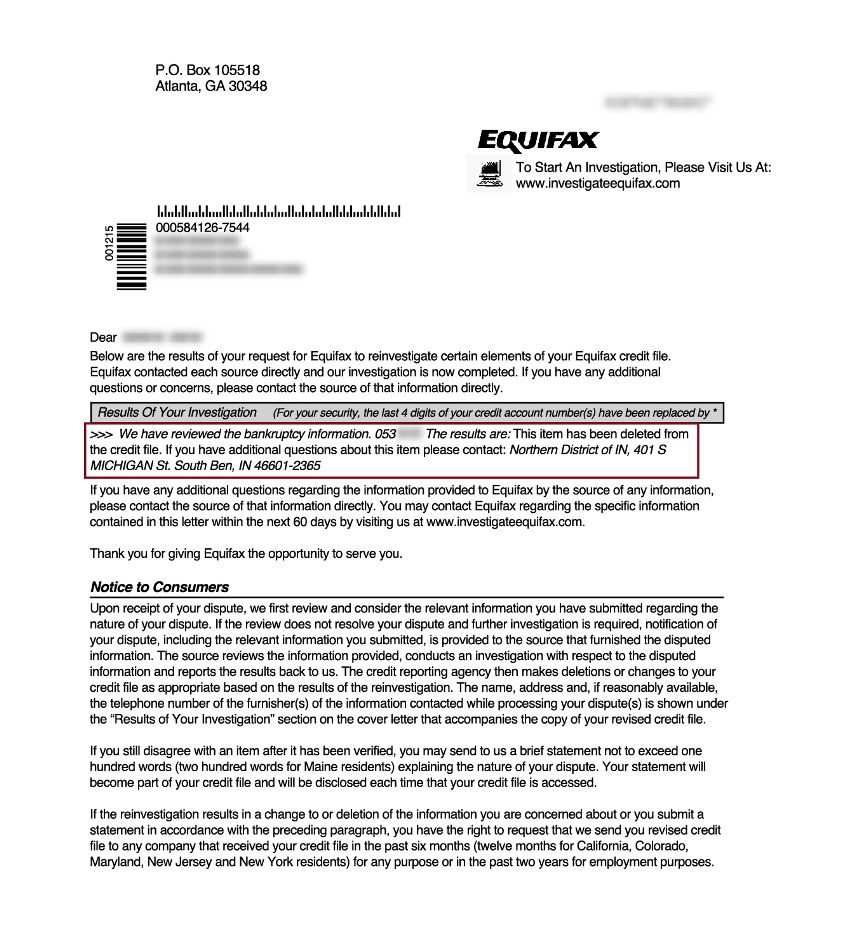

Bankruptcy Removed from Equifax:

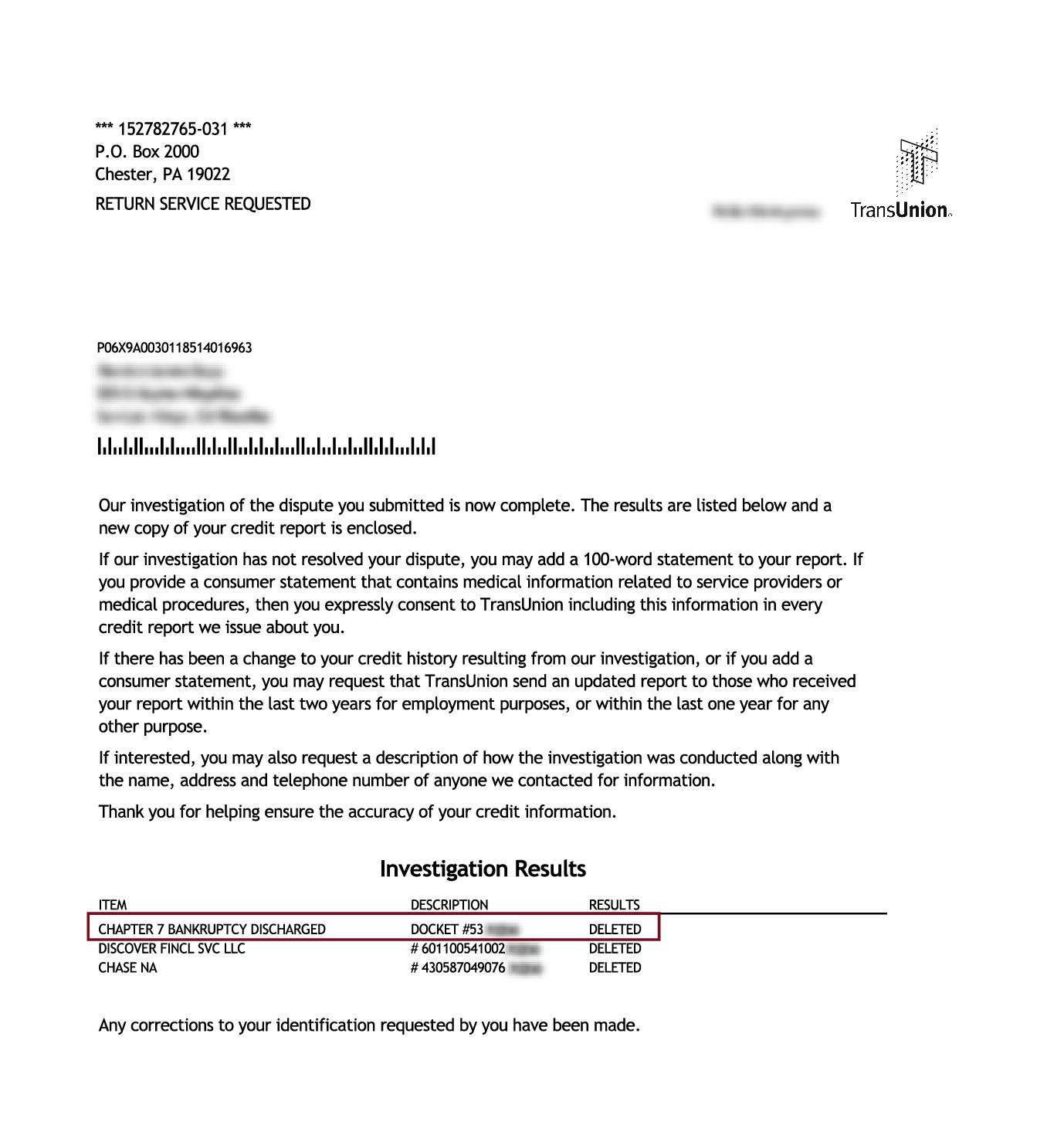

Bankruptcy Removed from TransUnion:

Charge-Offs Removed:

Start Your Credit Repair Journey Today

If you’re dealing with bad credit and need professional guidance, consider a free credit consultation with Credit Saint. They have a proven track record of helping people in similar situations, and their skilled team could provide the insight and assistance you need.

To get started, simply fill out the form on their website to see what they can do for you. Remember, the journey to a healthy credit score isn’t a sprint but a marathon. Having professional support along the way can make the process less daunting and more efficient.

Ready to Repair Your Credit?

Learn how to get help disputing errors on your credit report that could be hurting your credit score.