Did you know that more than 500,000 Americans declare bankruptcy each year? While unfortunate, it’s helpful to know that you are not alone when dealing with bankruptcy.

Even after your bankruptcy is discharged, there is the aftermath to contend with as well, namely, repairing your credit.

With so many people experiencing bankruptcy and so much financial data going through the credit bureaus, the chance for error is great. In fact, negative items can appear on your credit report from mistaken identity, identity theft, administrative mistakes, or reporting errors.

That’s why you must review all of your credit report information for accuracy, particularly the data surrounding the specifics of your bankruptcy.

We’ll walk you through why it works and what to do so you can start repairing your credit today, even with a bankruptcy in your past.

Ready to Raise Your Credit Score?

Learn how credit repair professionals can assist you in disputing inaccuracies on your credit report.

How long does a bankruptcy stay on your credit report?

The length of time you’ll see a bankruptcy stay on your credit report depends on what type it is. For example, a Chapter 7 bankruptcy stays on your credit report for 10 years from the date the bankruptcy was filed. On the other hand, a Chapter 13 bankruptcy remains on your credit report for just seven years from the filing date.

However, contrary to popular belief, you can remove a bankruptcy from your credit report early, and you can get credit after a bankruptcy. You do NOT have to wait seven or ten years after the bankruptcy filing date to get a mortgage, car loan, or any other type of credit again.

In fact, it usually only takes a couple of years to get access to loans and credit cards again. However, once you do start to qualify again, you may be paying extraordinarily high interest rates.

Rather than getting stuck with high interest rates and low balance maximums, work on negating the effects of bankruptcy as much as possible. Then, by disputing the bankruptcy and taking action to rebuild your credit history, you can get much better credit card and loan offers.

One mistake doesn’t have to set you back financially for the next ten years. Find out how to remove a bankruptcy from your credit report and other ways to recover from bankruptcy.

Accounts Included in the Bankruptcy

After you’ve filed for bankruptcy, the accounts included in your bankruptcy will show up as “included in bankruptcy” on your credit report. Most of them will remain on your credit report for up to seven years from the original delinquency date.

These include accounts like charge-offs, collections, repossessions, and judgments. They can also potentially be removed from your credit report before the reporting limit of seven years.

How does a bankruptcy affect your credit score?

Having a bankruptcy on your credit report can be devastating to your credit scores. According to FICO, for a person with a credit score of 680, a bankruptcy on your credit report will lower your credit score by 130-150 points.

For a person with a credit score of 780, a bankruptcy will cost you 220-240 points. Your credit score will drop several categories lower after that one event. The higher your credit score is, the more it falls.

You may not be eligible for future loans or credit cards, and if you are, you’ll most likely end up paying much higher interest rates. Furthermore, the amount you can borrow will probably become limited.

While filing for bankruptcy may be the best financial decision at this point in your life, it’s important to understand how and why it affects your credit score.

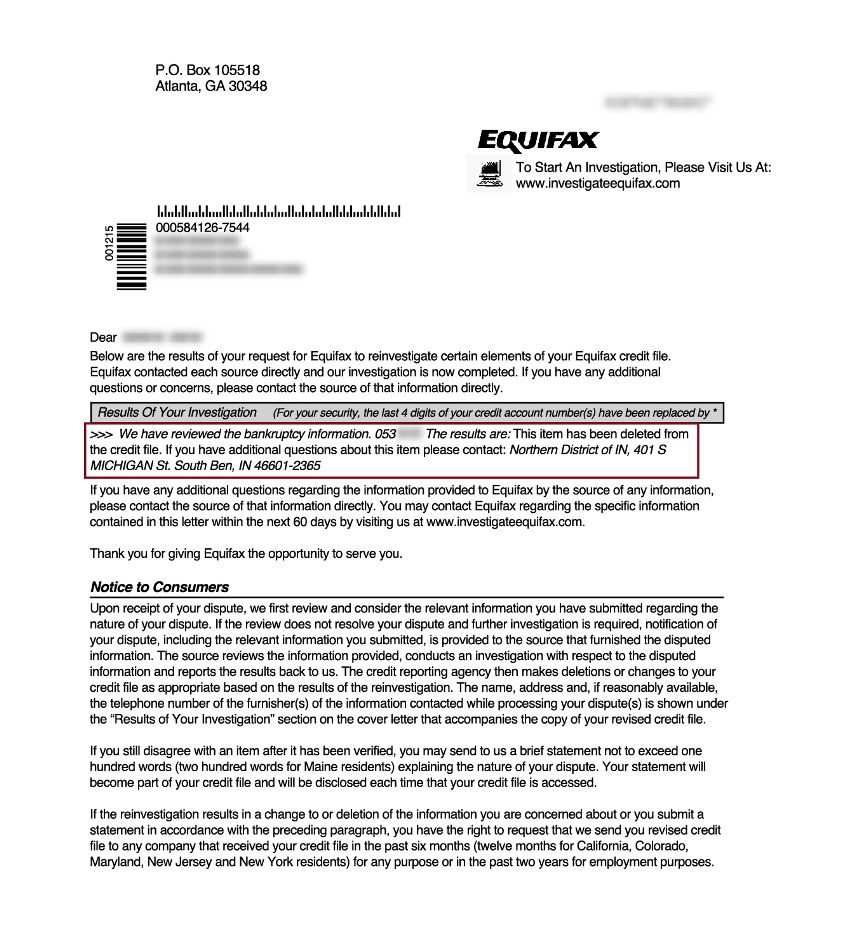

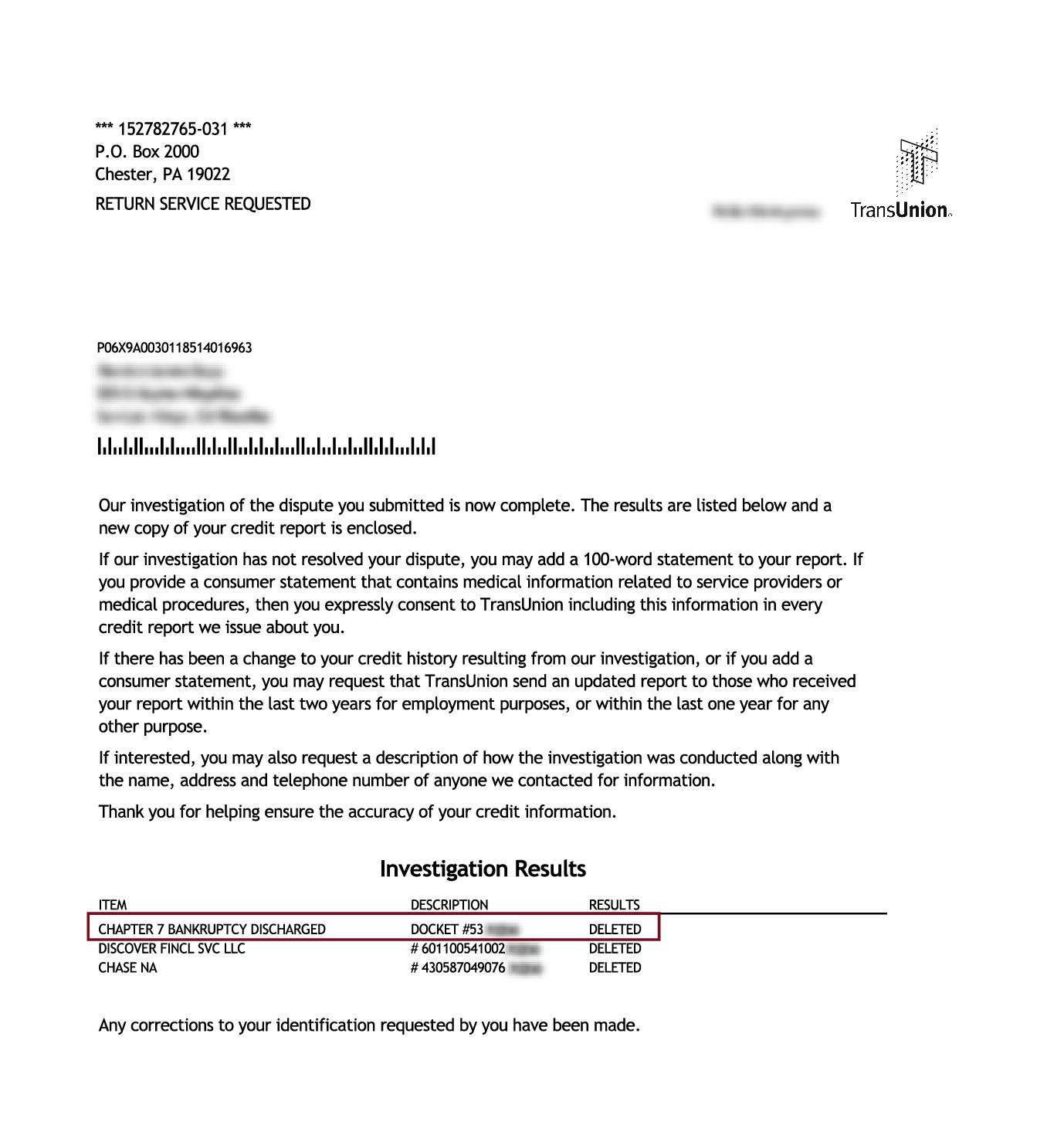

How to Remove a Bankruptcy From Your Credit Report

The first thing you want to do is grab a copy of your free credit report from each of the three major credit bureaus; Equifax, Experian, and TransUnion. You can do this at AnnualCreditReport.com. You are entitled to one free credit report every 12 months.

When disputing a bankruptcy, you’ll need to write a credit dispute letter to each of the three credit bureaus. Make sure the wording of your dispute doesn’t make it sound frivolous. Stick to the facts, and don’t get emotional. Sometimes, the less you say, the better.

Yes, you have certain protections under the Fair Credit Reporting Act (FCRA). However, the credit bureaus also have protocols in place to shut down consumers who don’t have legitimate disputes.

Remember the burden of proof is on the credit bureaus and they have 30 days to prove it. If they can’t, it must be removed from your credit report.

Once you’ve sent your letters to the credit reporting agencies, you’ll typically have to wait about 3-4 weeks for a response. If the bankruptcy doesn’t get removed, you can try sending a follow letter or consider hiring a professional.

How can I rebuild my credit after bankruptcy?

The most important thing you can do to improve your credit score after a bankruptcy is to remove the bankruptcy from your credit report.

Equally important is learning and changing your personal finance habits so that it doesn’t happen again. This might involve reviewing your income and expenses or building your emergency fund to prevent future financial hardships.

The most essential ongoing habit you can begin is to pay all of your bills on time because your payment history accounts for the largest portion of your credit score. Even a single 30-day late payment can cause a significant dip. So, imagine how bad it could be if you regularly miss a payment.

Your other best bet for rebuilding your credit after bankruptcy is to avoid accruing new debt.

Depending on the type of bankruptcy filing, you probably had much of your debt discharged. So, even though the bankruptcy itself is a major negative item on your credit report, consider the rest a blank slate.

Avoid racking up additional debt because that also has a significant impact on your credit score.

You may also want to get a secured credit card. It’s a credit card designed for people who want to rebuild credit history. The credit card issuer will give you a credit limit based on the security deposit you pay upfront. By making monthly payments on time, you can start to rebuild your credit immediately.

Can you remove a bankruptcy on your own?

Like all negative item disputes, it’s entirely possible to complete the process on your own. However, removing a bankruptcy from your credit report early can be a lengthy and tedious process that doesn’t guarantee results.

You can dispute the bankruptcy either by stating an inaccuracy of the information on your credit report or by asking the credit bureau how it verified your bankruptcy. As with any dispute, they must respond to your procedural request letter within 30 days.

In most cases, they’ll say that they verified it with the courts, but this is unlikely. So, you must then contact the court to ask how they verified your bankruptcy.

If they respond that they never verified it, you should get that statement in writing. Then, send it to the credit bureau, and ask them to remove the bankruptcy. This method isn’t guaranteed, but it might be worth trying. Otherwise, enlist the help of a credit repair company to manage the process for you.

Credit repair companies are highly experienced at disputing negative items on credit reports. They specialize in getting bankruptcy filings deleted from your credit report. Credit repair services also work to remove other negative information included in the bankruptcy, like charge-offs and collections.

Get Your Bankruptcy Removed Today!

If you’re looking for a reputable credit repair company to help you dispute and potentially remove your bankruptcy, consider working with Credit Saint.

Fill out the online form on their website for a free credit consultation. They have helped many people in your situation and have paralegals standing by waiting to take your call.

Chapter 7 Bankruptcies Removed

Ready to Repair Your Credit?

Learn how to get help disputing errors on your credit report that could be hurting your credit score.