How does a tax lien affect your credit?

As of April 2018, tax liens no longer affect your credit score. All three major credit reporting agencies decided to drop tax liens from their reports. However, an unpaid tax lien can lead to tax levies – where the government comes in and seizes your property to satisfy your tax debt.

This means you could lose your bank account, your car, or even your home if the tax debt is large enough. So, while tax liens no longer directly affect your credit history, they can still have a major impact on your finances.

How long does a tax lien stay on your credit report?

State and federal tax liens no longer appear on your credit reports. Before April 2018, paid tax liens remained on your credit report for seven years from the date it was filed and unpaid tax liens remained indefinitely.

Ready to Raise Your Credit Score?

Learn how credit repair professionals can assist you in disputing inaccuracies on your credit report.

Understanding Tax Liens

Tax liens are similar to civil judgments in that they are a legal remedy for your creditors to collect money from you. However, with a federal tax lien in place, the IRS establishes that they have a legal right to your property. This includes:

- Real estate you own – houses, land, etc.

- Personal property – your cars, jewelry, etc.

- Business property – any business property as well as accounts receivable (if you own a business)

- Financial assets – your bank accounts, retirement accounts, etc.

Having a federal tax lien makes it almost impossible to sell your home or qualify for new credit. The lien takes precedence, so when you try to sell your home, the purchase price must be used to satisfy it. This is a deal that few buyers will agree to.

Tax liens can easily turn into levies, and the IRS has already established that it is “first in line” to collect. So, creditors know that they won’t have much recourse if you default in the future.

The longer the debt goes unpaid, the greater your risk of being levied and having your property and assets seized.

Negative Impacts of a Tax Lien

As mentioned above, tax liens can create several big problems if left unaddressed. Let’s take a more detailed look at the potential issues that a tax lien could create:

Attached to All Assets

A federal tax lien represents a significant risk to any and all of your assets. Everything you own, from bank accounts, vehicles and real estate, or anything you acquire while the lien is in effect, can be seized.

Limits New Credit

While a federal tax lien shouldn’t show up on your personal credit report, it is still a matter of public record. As such, any potential lenders can see it. On top of that, the IRS will notify existing creditors that they have first claim on your property.

What this means is that it is extremely unlikely that any creditor will want to provide you with additional credit. Taking out a loan to pay off your tax lien probably won’t be an option, for example.

Affects Business Property

Keep in mind that an IRS lien will also put any business property you own at risk. This includes accounts receivable, so if you’re a business owner a tax lien is exceptionally risky.

Won’t Discharge After Bankruptcy

While successful bankruptcy can eliminate most private debt, it won’t necessarily protect you from an IRS tax lien.

How to Deal With a Tax Lien

Paying your tax debt in full is, of course, the easiest way to get rid of a tax lien. Ideally, you can pay it off in a lump sum, but there are also short and long term payment options offered by the IRS.

If you sign up for a short term payment plan, you will be required to pay the full amount owed within 180 days, or about six months. Short term payment plans don’t come with any setup fees.

With a long term payment plan, you will make monthly payments after payment a setup fee of $31. You can also opt in to direct debit payments which are automatically taken from your checking account each month.

Once your entire debt is paid in full, the IRS will release your tax lien within 30 days and you’ll no longer have to worry about the risk of assets seized.

If paying your debt in full isn’t possible even with a payment plan, you can consult the IRS website for more information. Depending on your situation, and how long your tax lien has been established, there may be more options available.

How to Remove a Tax Lien From Your Credit Report

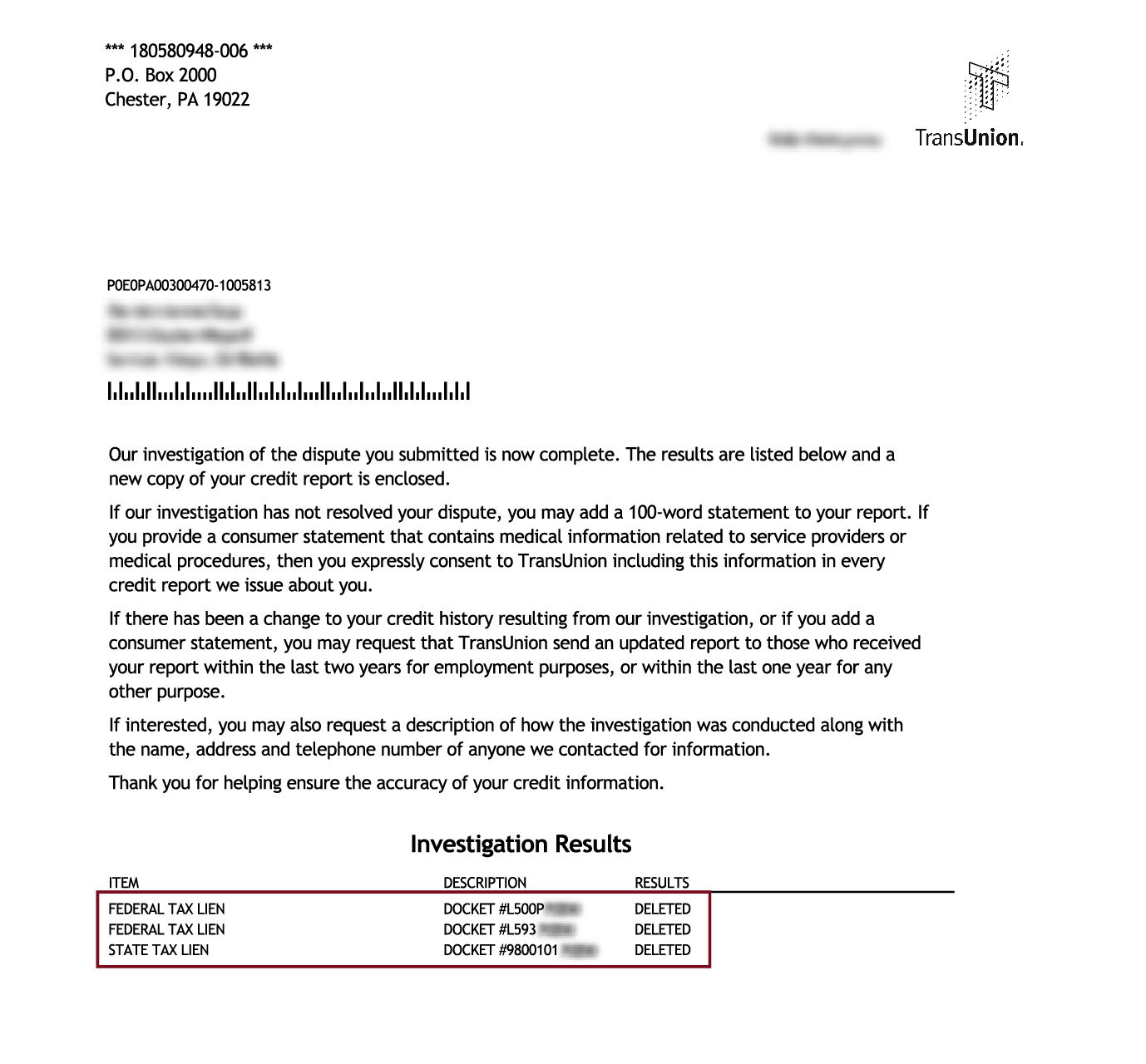

Tax liens are not supposed to be on your credit reports anymore. However, if you still see one on your credit report you have the right to dispute it under the Fair Credit Reporting Act (FCRA).

You also have the right to dispute other inaccurate information on your credit report that is questionable. Some items you can dispute include bankruptcies, foreclosures, repossessions, charge offs, judgments, tax liens, collections, late payments, and more.

If you notice any inaccurate information on your credit report, it’s best to file for a dispute right away. It’s relatively easy to raise a dispute directly with the relevant credit bureau.

If your dispute is denied, there are options for further action. For example, you could file a written statement that can be included in your credit report for future creditors to notice. You could also submit a complaint to the CFPB and contest the decision.

Working with a Professional Credit Repair Company

It’s often best to work with a professional that works with three major credit bureaus and creditors every day. There is help available if you are unsure exactly how to remove a tax lien or other negative items from your credit report.

Get in touch with the credit repair professionals at Credit Saint. They can deal with the back and forth with the credit bureaus for you. They can also help you improve your credit scores and have peace of mind knowing that you have the best chance of getting it removed.

Remove Your Tax Liens Now!

If you’re ready for a fresh start, let the professionals at Credit Saint take care of it for you.

Ready to Raise Your Credit Score?

Learn how credit repair professionals can assist you in disputing inaccuracies on your credit report.

Tax Liens FAQ

How do I know if I have a tax lien?

You can access your tax records online to check if you have a federal tax lien against you. If you don’t already have one you can open an online account with the IRS. There you can view your balance, create payment plans, and access any communications you’ve received from the IRS.

What is the difference between a tax lien withdrawal and a tax lien release?

After the IRS has filed a notice of intent to list a federal tax lien, there is a short window of opportunity where it can be withdrawn. This means the lien doesn’t officially make it to public records. A lien is usually withdrawn only when the taxpayer has begun to repay their tax debt.

A tax lien release is simply the process by which the IRS removes the lien once the debt has been fully paid. Unlike a withdrawal, a release occurs only the lien has been officially filed.

What is the difference between tax liens and levies?

While you might see the words lien and levy used interchangeably, they actually refer to two different tax collection measures.

A tax lien is a legal claim filed by the IRS to ensure its ability to collect taxes which are owed.

A levy, on the other hand, is when the equivalent of owed taxes are seized. The IRS defines a levy as the legal seizure property to satisfy a tax debt. This could include wages, bank accounts or any other property or asset.

Do tax liens impact your credit score?

Because tax liens are no longer included in your credit report, they can’t affect your credit score. However, tax liens are a matter of public record and as a result will directly impact your creditworthiness.

Any lender can search for tax liens when evaluating your credit or loan application. This means it is highly unlikely to be approved for a loan or new credit if you’ve got a tax lien against you.