Despite reported upswings in the housing market, foreclosures continue to be a big problem for residents of the US.

Regardless of the circumstances, dealing with a foreclosure is one of the most challenging situations a person can face. The stress of losing a home is only compounded by the damage foreclosures do to your ability to recover financially.

Foreclosure leaves a trail of poor credit, which means higher insurance and loan costs, assuming you still qualify.

How long does a foreclosure stay on your credit report?

Once you fall behind on your monthly mortgage payments by at least 120 days, your lender will begin foreclosure proceedings. After the proceedings begin, the mortgage lender usually reports the foreclosure to the three major credit bureaus; Equifax, Experian, and TransUnion.

The foreclosure will typically show up on your credit reports within 30-60 days. A foreclosure stays on your credit report for seven years. It will negatively affect your credit for up to seven years, but less as time goes on.

Can a foreclosure be removed from your credit report?

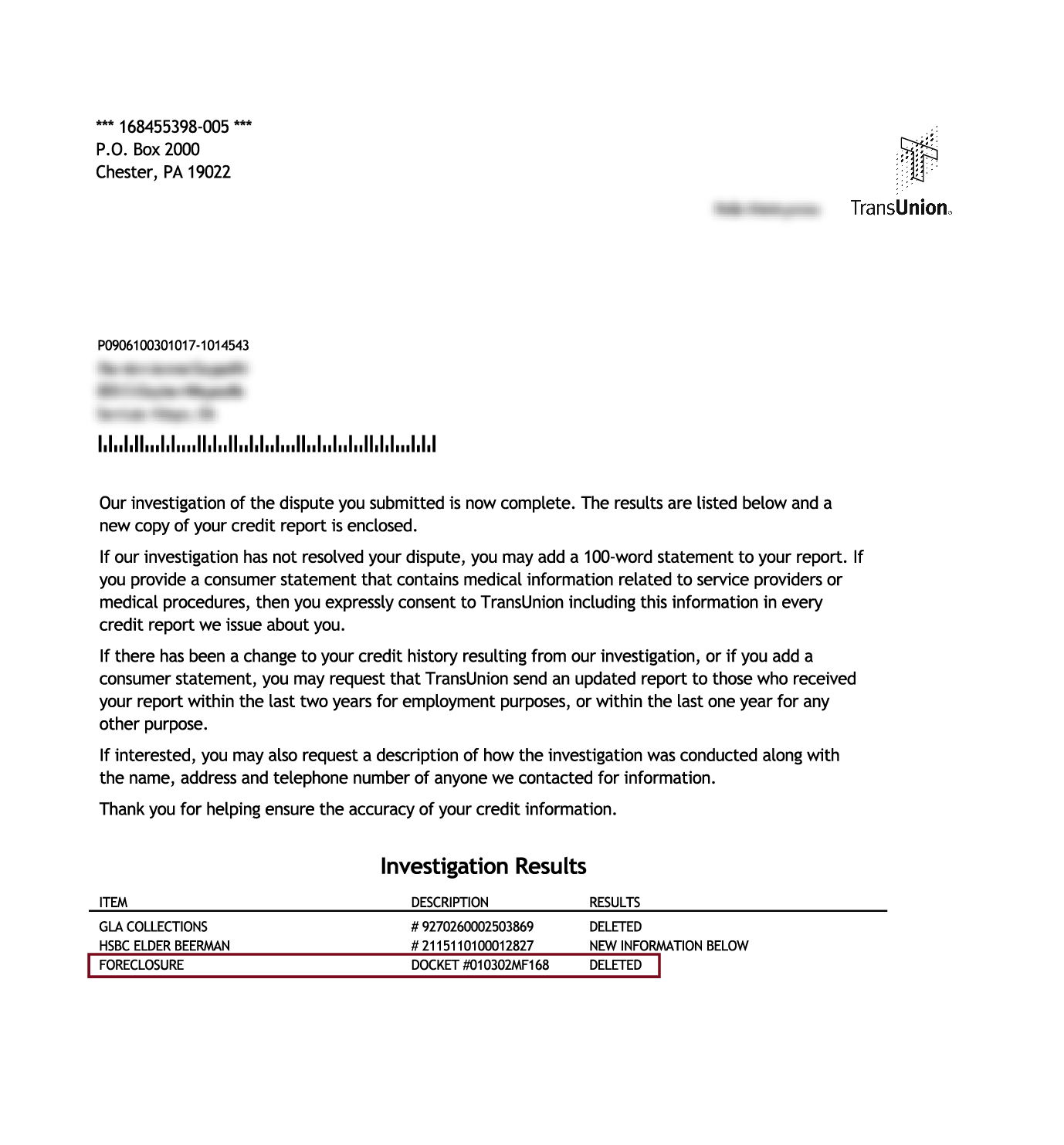

Yes, it is possible to have a foreclosure removed from your credit reports. The mistakes made by mortgage lenders have been well documented in foreclosure cases. Some banks have even had to restitution for mismanaged foreclosures.

Many errors have occurred in foreclosure cases, including the “rubber-stamping” of foreclosure documents and lack of proper procedure. For reasons such as those, it may be possible to have your foreclosure permanently removed. But, even if you deem a listing on your credit report as “questionable,” you can dispute it. The burden of proof is on whoever reported the item on your credit history.

Another common reason to have them removed is a lack of available records. This most often occurs when the bank that owned the mortgage loan is no longer in business.

In many instances, mortgages and foreclosures were sold from one bank to the next. This left a snarl of paperwork that made it impossible for people to pay their mortgages on time.

These sales also made it difficult for some banks to keep accurate records. Additionally, if the bank listed on your credit report is no longer in business, they will not be able to verify the foreclosure. Any information on your credit report that the credit bureau cannot verify must be removed.

How can I remove a foreclosure on my credit report?

If you would like to attempt the removal process of your foreclosure on your own before you contact a professional, there are two methods to use.

Step 1: Find Errors on the Credit Report Listing

First, grab a copy of your free credit report from each of the major credit bureaus; Equifax, Experian, and TransUnion. Once you have copies of your three credit reports in hand, look at each detail of the foreclosure entries.

Check the foreclosure balance, any dates associated with the account, your account number, and the name of your mortgage lender. If you find any of the information to be incorrect or questionable, you can dispute it.

Another big mistake to avoid?

Don’t assume that all three credit report entries are the same. There are three credit reporting agencies that compile information in different ways. Check each one for inaccurate information.

If you find an error concerning the foreclosure, you can file a dispute with all three credit bureaus. First, send a dispute letter, and you should receive a response within 30 days. Within that time frame, the credit bureaus need to verify the information within the entry and correct it, or ideally, remove it altogether.

Step 2: Write to the Lender

Another tactic you can take if the credit bureaus won’t remove the foreclosure is to write directly to the lender. Request that they remove the entry from your credit report due to inaccuracies and give them a 30-day deadline.

If they can’t verify or just don’t want to spend the time doing so, they might remove it altogether.

Step 3: Get Professional Credit Repair Help

Removing a foreclosure from your credit report requires filing separate disputes with all three credit bureaus.

Because of how credit reporting agencies work, you have to word your disputes carefully to avoid having them deemed “frivolous.” The Fair Credit Reporting Act (FCRA) offers protections for consumers. However, the credit bureaus have the right to ignore anyone that they feel is abusing the law.

The credit bureaus decide whether a dispute is frivolous solely based on your communication and any proof you can provide. This is one of the reasons many people hire a credit repair company to repair their credit and remove foreclosures from their credit reports.

If you have a foreclosure on your credit report, you may want to consider working with a reputable credit repair company like Credit Saint. They will give you the best chance of getting it removed.

Credit Saint can also help you potentially remove late payments, charge-offs, collections, repossessions, and even bankruptcies. If you’ve been struggling with bad credit and are ready to improve your credit scores, fill out the form on their website to see what they can do for you.

Ready to Raise Your Credit Score?

Learn how credit repair professionals can assist you in disputing inaccuracies on your credit report.

How does a foreclosure affect your credit?

Your credit score can drop from 85 to 160 points when a foreclosure first appears on your credit report. If your credit score was good to start with, expect a much sharper drop than if your credit was already poor or average.

In most cases, you will not be able to qualify for a new credit card, auto loan, or mortgage immediately after a foreclosure. In addition, you may also see the interest rates on your current credit cards rise due to the drop.

How does a short sale impact your credit?

In the past, you could reduce the damage of foreclosures by completing a short sale or deed-in-lieu of foreclosure rather than proceeding with an “official” foreclosure. However, the credit reporting agencies have since started penalizing all three of these situations identically.

The only potential benefit of a short sale or deed-in-lieu is the possibility of qualifying for a new mortgage soon after. However, the negative impact on your credit score may make this impossible.

Can I buy a house after foreclosure?

You won’t be able to qualify for a new mortgage for at least 2 years after foreclosure. This is the case even if you have the financial means to pay for a less expensive home.

Once you do qualify for a mortgage, expect to have to pay more in interest and fees. Additionally, you’ll likely need a much higher down payment—somewhere around 20% or more.

How long does a short sale stay on your credit report?

As mentioned above, short sales aren’t treated any differently from foreclosures, so they will remain for seven years as well.

What are some other ways that foreclosures can cost you?

Many people don’t realize the different ways your credit score impacts your everyday life. Along with access to loans or credit cards, your credit score is often used:

- As part of the hiring process – to weed out candidates with low credit scores

- To set insurance rates – to charge higher rates for poor credit or to disqualify people entirely

- To get approval for utilities – to charge hefty deposit fees to establish service

- For other services – for services such as cable and internet, you may not even qualify for service if your credit score is too low

It is also very common for landlords to run a credit check when screening potential renters.

Landlords usually weed out people with a poor credit score as a potential risk for nonpayment of rent. Unfortunately, this can make it almost impossible to qualify for a good home or apartment in a safe neighborhood.

Having a foreclosure on your credit report can make it even harder to find a place to live. Unfortunately, many people don’t realize that until they’re already looking for a home or apartment.

Large deposits will likely be required to establish necessities such as electricity, water, and garbage collection. This makes it even more difficult to start over and begin rebuilding your life after foreclosure.

Foreclosure Removed From Credit Report

Ready to Repair Your Credit?

Learn how to get help disputing errors on your credit report that could be hurting your credit score.